Religious Conversion

A former climate shareholder activist hedge fund changes its religion with the help of an American energy major.

“When it is a question of money, everybody is of the same religion." - Voltaire

With all due disrespect to Stanford civil engineer Mark Z. Jacobs and “renewable” energy fans like him, Big Tech was never going to rely on any combination of Spinning Green Crucifixes™ (wind), solar, and batteries to provide the 8,760 annual hours of always-on electricity on which its AI bets rely. While they may be faster to deploy, Big Tech isn’t betting trillions of dollars over the next few years on any source that can’t generate the juice for more than half the hours in a day, and battery systems can’t economically eliminate that problem, even if they don’t spontaneously combust.

So, in April 2024 when we posted Nat Gas & Nuclear’s New BFFs, predicting natural gas and nuclear would be the horses Big Tech would ride for their energy requirements, it was not exactly a trail-blazing prediction. Nuclear takes a long time to build. It was more like a James Carville, Captain Obvious moment: It’s the economy (natural gas), stupid.

Ever since we penned that post, our Big Tech Overlords have rushed around the country to secure dispatchable, reliable, affordable electricity in gargantuan amounts, prior big talk about “sustainabilchemy” and waterfalling cash at “Renewable Energy Certificates” (RECs) be damned. (We would be lying if we did not admit feeling a bit of schadenfreude.)

Without apologizing for the obvious flip flop and green hypocrisy, Big Tech could not have done a better job pissing off and alienating their former “environmentalist” allies. Those former allies have honed in on data center energy use, water use, and rural land conversion.

And worse: They view Big Tech lining up with natural gas and nuclear instead of “renewables” as a blatantly hypocritical religious apostasy, and the purchase of all those billions in RECs to burnish their corporate “sustainability” reports as disingenuous. The green crowd cheered for wind, solar and the spontaneously combusting mineral boxes with the docile sounding name of a pasture Hereford - “BESS” (“battery energy storage systems”) – but was instead left sitting in chairs against the wall at the big dance looking forlorn. And angry.

Most of those jilted, angry green forces are now lining up against their former technology heroes. The former defenders of eminent domain in landmark cases like Kelo vs. New London have suddenly become staunch defenders of property rights. Water use, CO2 emissions from gargantuan energy consumption, and rural land and environmental conservation – all very real data center proliferation concerns – already fit nicely in their wheelhouse.

Big Tech’s speaks through its actions. And if those actions were words, their response to the “renewables” crowd is essentially what Robert Bryce’s said in a recent post about the wind industry getting crushed, stalled, scattered, smothered, and covered by the Trump administration: “Cry me a fucking river.”

Elon Musk sent the message blatantly. While we were writing Nat Gas & Nuclear’s New BFFs, he was in negotiations to secure ~150 – 300 Megawatts (Mw) from Memphis Light, Gas and Water (which sources electricity from Tennessee Valley Authority) for his Colossus I and II xAI facilities outside Memphis. But MLGW’s and TVA’s processes do not move at sufficient speed for Rocket Man.

So, he simply slapped up 62 (that we can count) industrial gas turbines - similar in principle to aircraft jet engines but optimized for stationary power generation - across the two locations, air and other permits be damned. The Southern Environmental Law Center did not like that very much. It sued the company this April.

For xAI, all revenue is essentially a derivative of electricity consumption, and regulatory fines represent a minor expense. As such Elon will pay the defense costs and any penalties and fines, make sure the facility has the power it needs, and never rely on wind, solar and batteries to provide the bulk of the electricity for Colossus I and II. End of story.

Most of the generators at the two Memphis xAI facilities were provided by a company called Solar Turbines. While you might not have heard the name, you probably know their parent: Caterpillar, renowned makers of heavy equipment used in mining, construction, and other industries, as well as industrial-scale power generators.

That’s right. Caterpillar - whose diesel-powered industrial machines consume copious amounts of hydrocarbons worldwide in service of critical industries - is cashing in on the west’s infatuation with “renewables.” Caterpillar is not a climate-obsessed shareholder activist hedge fund trying to get Exxon and Chevron to drop oil and gas for wind and solar. Their motive is simple: shareholder returns.

In September 2024, five months after our post, Microsoft announced a 20-year power purchase agreement (PPA) with Constellation Energy. The reported $16 billion deal restarts the 835 megawatt (MW) Three Mile Island Unit 1 nuclear reactor in Pennsylvania, shutdown in September 2019. Microsoft will effectively consume the full output at the renamed Crane Clean Energy Center when the reactor comes back online in the next couple of years.

The very next month, Google announced a 10-year PPA with small modular reactor (SMR) developer Kairos. Amazon (through its Amazon Web Service unit and/or venture capital arm) inked $700 million in investments in SMR designer X-Energy and signed agreements for future SMR generation with utilities Northwest Energy in Washington State and Dominion Energy near its existing North Anna nuclear power station in Louisa County, Virginia.

Existing nuclear power plant restarts, license extensions, new plant expansions at existing nuclear projects, and new advanced SMR design, funding, and commitments were announced across America. By the end of 2025, it was clear that Big Tech is nuclear energy and natural gas’ new BFF (emphasis ours):

Big tech companies signed contracts for more than 10 gigawatts of possible new nuclear capacity in the United States over the last year. Microsoft committed to a 20-year, 835-megawatt power purchase agreement to restart Three Mile Island. Google ordered up to 500 megawatts of small modular reactors from Kairos Power. Amazon invested over $20 billion converting the Susquehanna site into a nuclear-powered AI data center campus. Meta issued a request for proposals targeting 1 to 4 gigawatts of new nuclear generation.

And the party kept going in 2026. In January, Meta announced a deal to buy ~2.2 Gigawatts (Gw) of electricity from Vistra’s Perry and Davis-Besse nuclear power plants in Ohio, and an additional 433 Mw of incremental upgrades across two plants in Ohio and one in Pennsylvania over the next eight years. The company also announced deals for nearly 4 Gw of power from SMR firms Oklo and Bill Gates-backed Terra Power.

By mid‑2026, industry reports listed at least 13 announced nuclear data center deals in the U.S., totaling ~10 Gw of nuclear capacity. The projects are all either contracted or targeted by the “big four” hyperscalers: Microsoft, Google, Amazon, and Meta.

But nuclear energy takes time to deploy. And as Elon demonstrated, Big Tech needs power faster than either the darling SMR developers or any traditional western nuclear firms can deliver Gw-scale existing designs like the AP-1000 units Georgia Power built at Plant Vogtle (where time and cost performance we less than inspiring).

So natural gas was always going to be Big Tech’s other energy BFF. And that’s why an American energy major’s announcement this week was nothing more than the logical culmination of events we foresaw. The timing likely got a boost from that little something that someone did in Iran the last four months.

What was notable about the announcement was not so much that it was another example of Big Tech abandoning any pretense that its own energy demands could be met with “renewables” and instead cutting a long-term deal relying on natural gas. More noteworthy was the fact an American evoil™ major’s new bespoke natural gas project for Microsoft has a partner you’d least expect: a former hero and darling of the climate shareholder activism industry, a hedge fund who only four years earlier had successfully targeted its biggest competitor and had its guns aimed at its newly announced partner next.

Which American energy major announced a first-of-a-kind data center project for its industry this week? Who is its new partner with the pedigree so counter to the project’s central strategy that on a list of ten likely firms, it would have been #99?

Get your boots out, we’re going to the Permian basin of west Texas. That’s where money, arbitrage, and the dynamics of the coproduction of methane with crude oil changed one “sustainability” minded hedge fund’s green religion to natural gas blue.

We begin the story with a brief explanation of the unique dynamics of hydrocarbon production in the Permian basin. Last April, an excellent Doomberg post summarized the situation nicely for our purposes (emphasis ours):

…there are now three categories of oil and gas producers in the world: those that produce only oil, those that produce only gas, and those that produce a mixture of the two. It is the rapid emergence of the third category - especially in the US, but increasingly in other countries as well - that has so disrupted the energy markets. Three-quarters of US crude oil and half of its natural gas are now produced concurrently, creating a classic co-product competition dilemma for single-product drillers.

Since the onset of this development, natural gas has been the nuisance byproduct in the U.S., routinely flared on-site or sold at steep discounts—a situation only worsened by OPEC’s efforts to prop up crude oil prices. When domestic gas prices sank to rock-bottom levels, producers in the gas-only fields of Appalachia and Haynesville were forced to curtail.

But not in the Permian basin of west Texas and southeastern New Mexico. There, the geology is more conducive to large scale coproduction than all other fields in the U.S. When crude oil market prices send the signal that oil is more valuable than natural gas, the gas becomes a “nuisance byproduct” in economic terms.

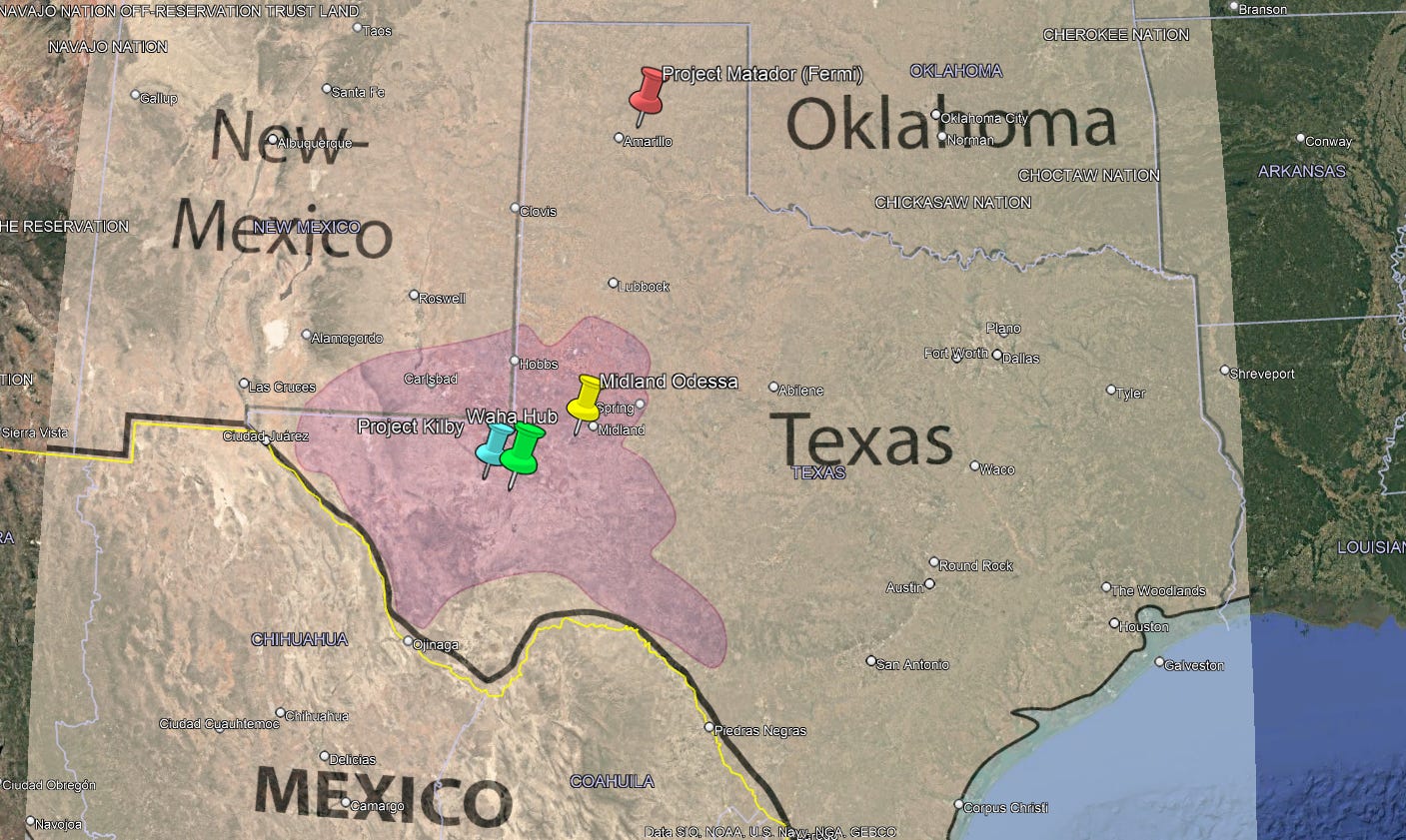

The Waha natural gas hub (the Waha hub) in west Texas’ Pecos County near the small, unincorporated community of Coyanosa is about 60 miles southwest of the Midland-Odessa metro area, the major business hub in the eastern Permian Basin. There, more than a dozen major interstate and intrastate pipelines intersect to transport gas to domestic markets and Mexico. Pipelines like the Gulf Coast Express, Permian Highway Pipeline, Whistler, and Matterhorn Express deliver Permian gas to Gulf Coast liquefaction facilities for export to international markets, and more are under construction and/or expanding.

Because of the coproduction dynamic, there have been several periods over the last few years during which natural gas at the Waha hub traded at negative prices for a number of days. More natural gas was being produced than could be piped out of the Permian basin, and the producers were either forced to pay someone to take it or flare it.

Just prior to Trump’s War in Iran, natural gas at the Waha hub set a new record for most consecutive days (13) trading at negative prices. Two weeks ago, natural gas spot prices at the Waha hub traded in positive figures for the first time in 90 days.

Left to their own devices, markets close arbitrages. The price of natural gas in west Texas eventually had to draw huge hyperscalers to the area. And with them speculative developers with big dreams … and other people’s money.

Enter Rick Perry, former Texas Governor and Energy Secretary during the first two years of Trump’s first term, a group of investors, and Fermi America (Fermi). The data-center real estate development and power company is attempting to build a private “HyperGrid” to serve hyperscalers, starting with 6 Gw natural gas, adding 4 Gw traditional large scale and advanced SMR nuclear, and ~1 Gw of the obligatory-for-optics solar panels and spontaneously combusting BESS pasture cows. Fermi describes its Project Matador as helping close the growing gap between AI’s voracious power demands and the public grid infrastructure’s ability to keep up with it.

Fermi controls the ~7,500-acre site in the Texas panhandle northeast of Amarillo owned by Texas Tech under a 99-year ground lease. It is adjacent to the U.S. Department of Energy Pantex industrial site, the nation’s primary facility for the assembly, disassembly, and maintenance of nuclear weapons.

As for progress, the website states that over 4 miles of natural gas piping are already in the ground, and more than 11 miles of site fencing have been placed around 300 cleared acres. The first shipments of combined cycle natural gas turbines and associated kit are reportedly on the way.

Fermi went public via Initial Public Offering on the NASDAQ in October 2025. The company sold ~ 32.5 million shares at about $21/each, valuing the company at over $15 billion. Market analysts framed Fermi’s Project Matador as something of a stress test for the “if you build it, they will come” model of hyperscale development, leveraging nearby Permian gas.

But the company and project have struggled ever since. After topping $30/share after the initial launch, the stock has been on a steady decline, trading below $4 in April and May this year after CEO Toby Neugebauer was ousted in a dispute that led to his suing the company. (It has recently bounced back to around $9.)

Recent coverage in legacy media does not paint a pretty picture. It describes a company that is still without customers, in pre-construction mode, with leadership turmoil and growing skepticism about whether Fermi can secure the financing, permits, and the anchor Big Tech tenants needed to turn Matador from an overhyped, overvalued “AI-nuclear campus” into a functioning energy and data-center complex.

On the surface, Fermi’s bet on cheap Permian natural gas would seem to be a solid bet, but its’ “if you build it, they will come” model is still very much in question given the project’s current status. And, as it turns out, Fermi wasn’t the only business eyeing the arbitrage between the U.S. Henry Hub benchmark price for natural gas and the recent negative pricing at the west Texas Waha hub.

This week, an American oil major with significant investments in the Permian basin announced a hyperscaler project. But unlike Fermi, they are not building on speculation.

Chevron is developing a power generation facility near Pecos, Texas, to provide electricity for a Microsoft data center under a 20-year PPA. “Project Kilby” is anticipated to deliver 2.67 gigawatts of capacity once build out is complete.

The announcement states that the agreement is a first milestone, with a final investment decision expected by year end. Chevron anticipates first power delivery in 2028.

With substantial production in the basin, Chevron is well positioned to leverage the recurrent bottlenecks at the Waha trading hub that result in negative pricing and flaring when production exceeds takeaway capacity. That situation is a direct function of the co-production of oil and gas in the Permian basin that Doomberg and others have noted, owing to its geology and the technological innovations in directional drilling and hydraulic fracturing (fracking).

Chevron’s project for Microsoft in the area may be the ideal Permian arbitrage play. By comparison, Fermi’s Project Matador looks more speculative than ever.

Project Kilby is a bespoke project developed by an American oil major who knows how to lay pipe and play energy arbitrage on scales for which Fermi’s executive team can only dream. Fermi’s Project Matador still does not have its first tenant.

It is worth considering what Microsoft’s choice might say about how the biggest hyperscalers like the ones mentioned above view Fermi’s “build it and they will come” model at Project Matador.

For a risk averse Big Tech giant like Microsoft, Chevron’s gas reserves and balance sheet virtually eliminate credit risk on a 20-year PPA. No mid-cap, speculative, private grid developer depending on third party pipeline capacity and long-term financing can match that.

Project Kilby is a co-located, dedicated, behind-the-meter campus, and effectively a power generation complex connected to a single, anchor tenant. It is precisely what Doomberg predicted more than a year ago due to the very arbitrage they kept noting between the benchmark U.S. Henry Hub and the Waha hub: gas goes in one end, data comes out the other, with none of it metered by or produced through the public grid.

Project Matador is a multi-tenant “hyper campus” (with no tenants) with one power generation complex serving multiple data center customers. Those customers will have to share power, infrastructure and to some extent governance with each other and Fermi. By comparison to Kilby, Matador is a giant hyperscaler co‑work complex with more expensive power and no single-tenant control.

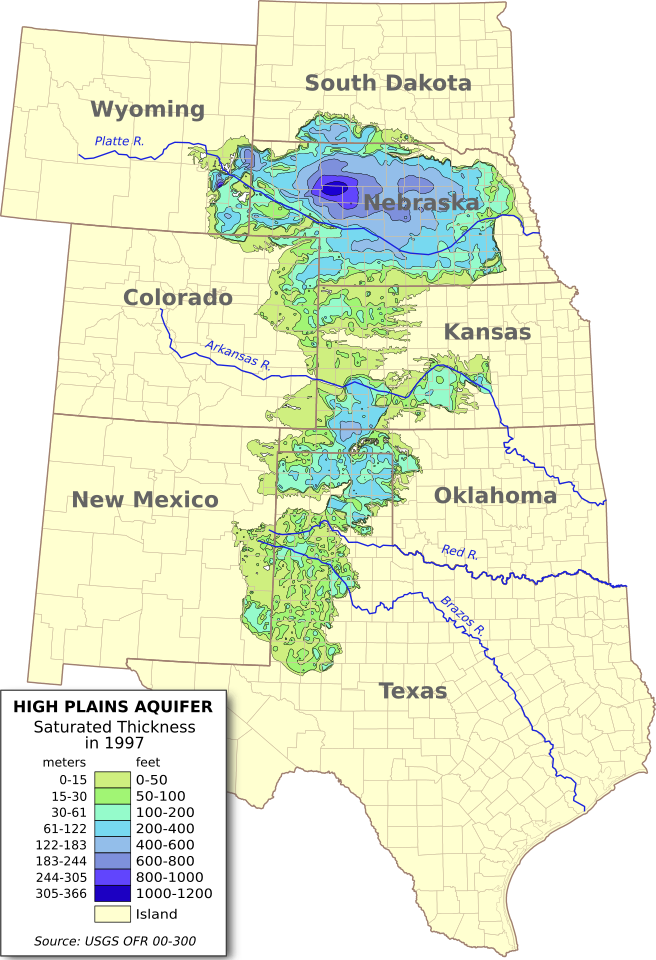

Kilby is in Reeves County near the city of Pecos. The two are positioning the area as a Permian energy industrial corridor, with visions of becoming a substantial industrial hub on the opposite (west) side of the basin from Midland – Odessa. The Project Matador site has more political complications. It sits next to the only U.S. nuclear weapons assembly/disassembly complex. It will use water, and the greatest saturated thickness and highest water quality in the Texas portion of the Ogalla aquifer sit under the site.

Project Kilby intends to use non-potable, brackish, low-quality groundwater for power plant operations. Chevron’s announcement states that it is “working to advance solutions for reuse of produced water from oil and gas operations,” potentially turning what is otherwise a costly expense for oil and gas producers in the Permian into either a smaller liability or maybe even a potential source of revenue someday.

In terms of reputational and regulatory risk/hassle, these things matter. Kilby is free of many political complications that face Matador. Anti‑nuclear, climate/environmental, and local‑community advocates are more likely to fight it than a more remote Permian gas plant in an area like Pecos where hydrocarbon infrastructure and natural gas power plants are about as common as tumbleweed, mesquite, and rattlesnakes.

Fermi has 6 Gw of air permits in hand. But it has no tenants and lacks full gas turbines and associate infrastructure procurement, financing, and connections for a project with energy ambitions almost an order of magnitude greater (17 Gw vs. 2.67 Gw). ZeroHedge reported that Chevron has already secured orders for seven GE Vernova gas turbines and supporting kit, a big deal given that most hyperscale data center developers and utilities are facing well-reported constraints due to multi-year backlogs for large gas turbines and related hardware.

At Fermi’s project, Microsoft would likely be one of multiple hyperscaler tenants in a seller’s market, with less control or ability to customize the infrastructure to its requirements. It would be less able to dictate commercial terms, reliability standards and impose its environmental requirements. Kilby makes Microsoft the anchor tenant and co-architect of the project, not just a tenant stuck with someone else’s plug-and-play mega campus.

Finally, as if all of these advantages were not enough, when you get right down to it, Fermi’s Project Matador is essentially a giant real estate development targeting hyperscale data centers with large electricity capacity. But as they say in real estate, location is everything, and here is where Project Matador is at a significant disadvantage relative to the power generation element.

We pinned the location of Fermi’s project on a Google Earth map with an overlay of the Permian basin. Fermi’s Project Matador is about 200 miles away from its center of production and the Waha hub. Existing natural gas pipeline capacity is insufficient to feed the ambitious project’s gargantuan future fuel appetite, and running new natural gas pipelines to the north side of Amarillo with sufficient capacity will be expensive.

The general location of Project Kilby near Pecos, Texas, as well as the Waha hub are shown, smack dab in the middle of the Permian basin. One would have to be blind not to see the inherent advantage of Chevron’s newly announced project simply by virtue of necessary length of required pipeline runs.

That matters commercially. At Project Kilby, Chevron can monetize local gas that would otherwise be heavily discounted at the Waha hub. Fermi’s Project Matador will require a much longer pipeline, sending the fuel further over constrained intrastate routes, adding cost and transport risk in a bottlenecked basin. Even with the new takeaway capacity that’s coming (not coming quickly enough), much of that gas is spoken for, headed east to Gulf Coast LNG liquefaction and export terminals. Other portions are headed west or even south, with less headed north to the Texas panhandle.

We find none of these differences particularly surprising given the way Microsoft and Chevron go about large investment decisions and deploy their own capital, versus a speculative developer using other people’s money like Fermi. What did surprise us was one of the participants listed in Chevron’s Project Kilby announcement, a name we immediately recognized from a post we wrote about two years ago (emphasis added).

Our February 2024 post Big Evoil Punches Back detailed Exxon’s successfully turning SEC’s rules constraining muckraking activist investors - FollowThis and Arjuna Capital - against them. As part of the story’s background, we began with a brief history of a climate shareholder activist hedge fund whose efforts against Exxon’s Board actually succeeded (emphasis added):

In December 2020, a newly formed activist investment fund called Engine No. 1 purchased $40 million worth of Exxon Mobil stock. Shortly after taking the position, its Founder Christopher James penned an open letter to the Exxon Board of Directors criticizing Exxon’s Return on Capital Employed (ROCE).

Continuing, we wrote:

Christopher James and Engine No. 1 chose a different tact than their predecessors. They successfully convinced some of Exxon’s largest shareholders, including (ESG Maven and) Blackrock CEO Larry Fink, Vanguard, and State Street, to vote for their proposal.

When the smoke cleared after Exxon’s shareholder meeting in May of 2021, despite holding a mere 0.02% of Exxon shares, Engine No. 1 candidates had won three seats on Exxon’s Board of Directors. The usual legacy media Climate Corps hailed the win as a transformational, “David beats Goliath” victory.

In summer 2021, after Engine No. 1 successfully went after Exxon, James pointed his gun at Chevron. So, the company met with Engine No. 1 leaders.

Chevron has recently met with representatives of activist investor hedge fund Engine No. 1 to talk about plans for emissions reductions, as the U.S. supermajor is getting ready for a possible proxy battle similar to the one Exxon led —and lost—earlier this year, The Wall Street Journal reported on Friday.

The meetings were described as “cordial.” Engine No. 1 did not indicate it would engage in an Exxon-style proxy battle at Chevron.

Chevron did not seem bothered. Why? The corporation said it had “contingency plans” to respond to many different types of events, including an activist investor.”

Only Chevron and the climate activist hedge fund led by Chris James know what was said in that, and subsequent, meetings. But suddenly, after the meeting with Chevron in summer 2021, Engine No. 1 seemed to be having a quiet change of heart despite its success winning the three seats on Exxon’s board, when the wind was actually in its sails. As we noted in that February 2024 post, it started pushing back on other climate activist proposals via its three board representatives (emphasis added):

For glaring examples of the divergence between the interests of Arjuna/Follow This and those of Exxon’s shareholders, look no further than Engine No. 1’s recent votes on such matters. In 2022, Engine No. 1 voted against Follow This’ shareholder proposal calling for Exxon to reduce its Scope 3 emissions. In October 2023, all three of Engine No. 1’s successful 2021 Board picks voted in favor of Exxon’s $60 billion acquisition of Permian basin oil and gas giant Pioneer Natural Resources.

What exactly was discussed in that fall 2021 meeting between Chevron and Engine No. 1? Why did they suddenly back off? What were the specifics of Chevron’s “contingency plans” for dealing with Engine No. 1?

As it turns out, we had inadvertently stumbled on to a thread. In the wake of Chevron’s formal announcement this week, Project Kilby seems to have answered those questions (emphasis added):

Chevron Corporation (NYSE: CVX) today announced that Energy Forge One LLC, a wholly owned subsidiary, has signed an agreement with Microsoft Corp. (NASDAQ: MSFT) to develop a co-located power facility in West Texas that will provide dedicated electricity to a Microsoft-operated data center under a 20-year power purchase agreement. Chevron and Engine No. 1 have been collaborating on the development, known as Project Kilby (“Kilby”).

Kilby is expected to deliver approximately 2.67 gigawatts of capacity, built through a phased, modular approach that enables incremental expansion over time. A majority of the generation will come from large GE Vernova (NYSE: GEV) turbines and associated electrical infrastructure, with additional capacity provided by Solar Turbines, a wholly owned subsidiary of Caterpillar Inc. (NYSE: CAT).

‘Ya don’t say!!

Now what could possibly have caused Engine No. 1 – a climate activist hedge fund that successfully forced its way on to Exxon’s Board of Directors and pointed its guns at Chevron next - to have such a change of heart?

Now that Chevron let the cat out of the bag, the answer seems clear. Clear enough that Engine No. 1 did not even try to pretend to hide it.

On the same day that Chevron released the announcement for Project Kilby noting its relationship with Engine No. 1, the latter released the following on its website (emphasis ours):

Joulent, LLC (“the Company” or “Joulent”) today announced its launch as a technology-driven energy company purpose-built to deliver reliable, multi-gigawatt power at the speed and scale demanded by the current pace of innovation. Founded and developed over three years by Engine No. 1 in strategic collaboration with GE Vernova, Joulent will provide reliable, continuous power engineered to meet the needs of American innovation.

“Leadership in the AI era will be determined by who can deliver energy and compute the fastest, most reliably, and at the lowest cost,” said Chris James, Founder and CEO of Engine No. 1 and Joulent. “By building new power generating facilities, Joulent enables customers across industries to power the next chapter of American innovation – while reducing pressure on existing grids and maintaining affordability for ratepayers.”

As Joulent’s first power project, Engine No. 1 and Chevron have been collaborating on a natural-gas power facility project in West Texas known as Project Kilby (“Kilby”).

Cynics might accuse Chris James and Engine No. 1 of selling out the hedge fund’s “sustainabilchemy” mission by collaborating with Chevron and Microsoft on a Gw-scale natural gas power plant complex. You can count us among them.

But don’t worry, the Joulent announcement gives reassurances that the green dream is still alive and well at Engine No. 1 (read: barely, on life support, and mostly for optics):

“The model also provides a foundation for future expansions through renewable energy sources, beginning with solar, creating additional pathways to add clean generation capacity over time.”

We close by noting that “climate change, greenhouse gases and sustainability” for years were the motivation for, and animated, Engine No. 1’s very existence. Today, all such terms are conspicuously absent from the born-again hedge fund website’s self-description. Funny that.

The Project Kilby announcement demonstrates just how deep the reckoning with physics and energy cuts where the rubber meets the road. The Big Tech darlings who purchased all those RECs to burnish their “sustainability” credentials abandoned the pretense that “renewables” could provide the power they need the instant the exercise changed from virtue signaling to earnings per share. It’s that simple.

What happened to Engine No. 1’s activist enlightenment? Is producing and combusting natural gas and its associated environmental and climate impacts now OK to the former climate shareholder activist? If so, is that only because some it would have otherwise been flared in the Permian? Or because it has nearly half the GHG emissions as oil?

Or is it really just because it is abundant, cheap, and the best arbitrage on the board for a hedge fund with money and understanding of how to play it the data center craze?

Or was Chevron’s “contingency plan” back in 2021 effectively telling Chris James and Engine No. 1, “We see what you did at Exxon. You won’t beat us, but you can join us”?

After such an amazing religious conversion, inquiring minds want to know. Meanwhile, from our perch, it sure looks like money can change a man’s religion from green to (natural gas) blue.

“Like” this post or we’ll sell you into slavery working for Engine No. 1.

Leave us a comment. We read them all and reply to most. Helps refuel the tank here.

environMENTAL is a reader-supported publication. We are free to all but please consider a voluntary paid subscription to show your support. Subscribe below.

Share this post. Helps us grow. We’re grateful for the assist!

Much to the dismay of the Ecofacsists and green grifters, Big Tech has learned the fundamental rule of life. Reality always trumps ideology.

Wow, the length and breadth of your scholarship is a sight to behold, Environmental. I am going to start a Tribute to you and your remarkable work.