Read My Lips

Contradictions do not exist. Whenever you think you are facing a contradiction, check your premises. You will find that one of them is wrong. – Ayn Rand

Saying one thing and then doing another causes the people on whom you count to question your character and integrity. After doing so, winning back their trust can be hard. The electorates of advanced Western nations have, unfortunately, come to expect this type of behavior from their Charlaticians™.

In an April post titled The Super Dupers, we reminisced about George H.W. Bush’s famous 1988 campaign pledge, “Read my lips, no new taxes”. In 1990 Bush, having backed himself into a corner, conceded to the Democrat controlled Congress and increased several existing taxes. In retrospect, many believe the opening he created for his GOP opponents - and ultimately for Bill Clinton - was his undoing.

Dramatically changing one’s position can be a sign of growth and maturity, or it can be a fast and sure way to make people question your motives, trustworthiness, and authenticity. George H.W. Bush got spanked by Bill Clinton in the 1992 Presidential election. The latter would go on to have his own issues with character, integrity, and trustworthiness.

The hype and overpromises of the ESG movement (Environmental, Social and Governance) were bound to result in some hypocritical contradictions and backpedaling. But the greenwashing optics and virtue signaling were just too sexy a public relations drug. Some corporations just could not stop themselves.

The consequences of the hyperbole are increasingly being exposed by the day. ESG and “renewable energy” appear to be on a collision course with physics and economics, aka “reality”. (Warning to queasy types: avert your eyes over the next few years.)

Over the last 18 months, the reality train hit Europe hard, especially Germany, in the wake of Putin’s invasion of Ukraine. But Germany in particular seems loathe to learn the lessons from the mess created by its self-inflicted “Energiewende” (“energy transformation”). Last week, German Minister for Economic Affairs and Climate Action Robert Habeck told his subjects that Germany faces five tough years ahead and revealed the country will have to borrow to support companies’ energy costs or lose their industry. Habeck stated:

“Tough years of green industrial transition will put a burden on people.”

All over the Western world, the cracks in the ESG story are beginning to show, including in some of the world’s largest companies. Across a variety of industries, comparing their words and actions from ~3 years ago versus today, it would be fair to ask, “what happened that caused the ‘E’ in their ESG positions to change so dramatically?”

In his 2020 letter to CEO’s, Blackrock CEO Larry Fink voiced the firm’s strongest emphasis on climate change to date. Fink’s letter mentioned climate risk pertaining to municipal infrastructure (bonds), the 30-year mortgage (flood/fire insurance), interest rates, food, inflation, and a host of other horrors. His letter noted (emphasis in original):

These questions are driving a profound reassessment of risk and asset values. And because capital markets pull future risk forward, we will see changes in capital allocation more quickly than we see changes to the climate itself. In the near future – and sooner than most anticipate – there will be a significant reallocation of capital.

(Prophetic, we believe. Just in the opposite direction he meant.)

In his letter to clients the same year, Fink stated (emphasis added):

We believe that sustainability should be our new standard for investing.

At the time of his 2020 letters, Blackrock was managing 5 of the top 20 “sustainable” funds by assets. Fink began to increase pressure on companies held in Blackrock’s funds to cut their carbon emissions and threatened to drop the “underperformers”.

But in August 2022, nineteen Republican state Attorneys General wrote a letter accusing Blackrock of sacrificing returns in favor of its ESG commitments. The firm faced mounting pressure for its ESG positions from Republican politicians. When a number of state Treasurers moved ~$1 billion dollars in state pension fund investments, Fink’s tune began to change.

By summer 2023, Fink sounded very different. According to a June 2023 Reuters article, he said "I don't use the word ESG anymore, because it's been entirely weaponized ... by the far left and weaponized by the far right."

When Blackrock named Amin Nasser, CEO of the Saudi State oil company Aramco, to its Board of Directors the next month, Larry Fink suddenly didn’t look like quite the same revolutionary “green” business leader that he had three years earlier. Saudi Aramco is effectively nowhere to be seen in “alternative energy”. Saudi Arabia has well-documented human rights “issues”.

If a U.S. asset manager wanted to add a Board member to intentionally thumb its nose at the “environmental” and “social” aspects of ESG, it could hardly make a better choice than Nasser. In an emailed statement to Bloomberg, Fink said Nasser’s appointment “provides BlackRock with ‘a unique perspective’ on key issues facing the company and its clients”. “Unique”, indeed.

Is Blackrock’s direction change merely a function of pressure from State Treasurers, Republican Charlaticians, and the “weaponization” of ESG? Or did the public ruckus merely give Fink and Blackrock a convenient “out” once the reality of physics and economics hit home?

Was Blackrock’s ESG “commitment” just more Wall Street greenwashing from the start? In a February post, we highlighted two of Blackrock’s “ESG” and “Sustainable” labeled funds in which Chevron and OneOK (a natural company) were the #5 and #6 holdings.

Two of the world’s largest energy companies seem to have similarly marched themselves into a box canyon, only to retreat once they realized the path ahead was an insurmountable canyon wall. In another episode of ironies abound, one of them did so after having been dragged before a Dutch court by environmentalists and ordered to reduce its CO2 emissions.

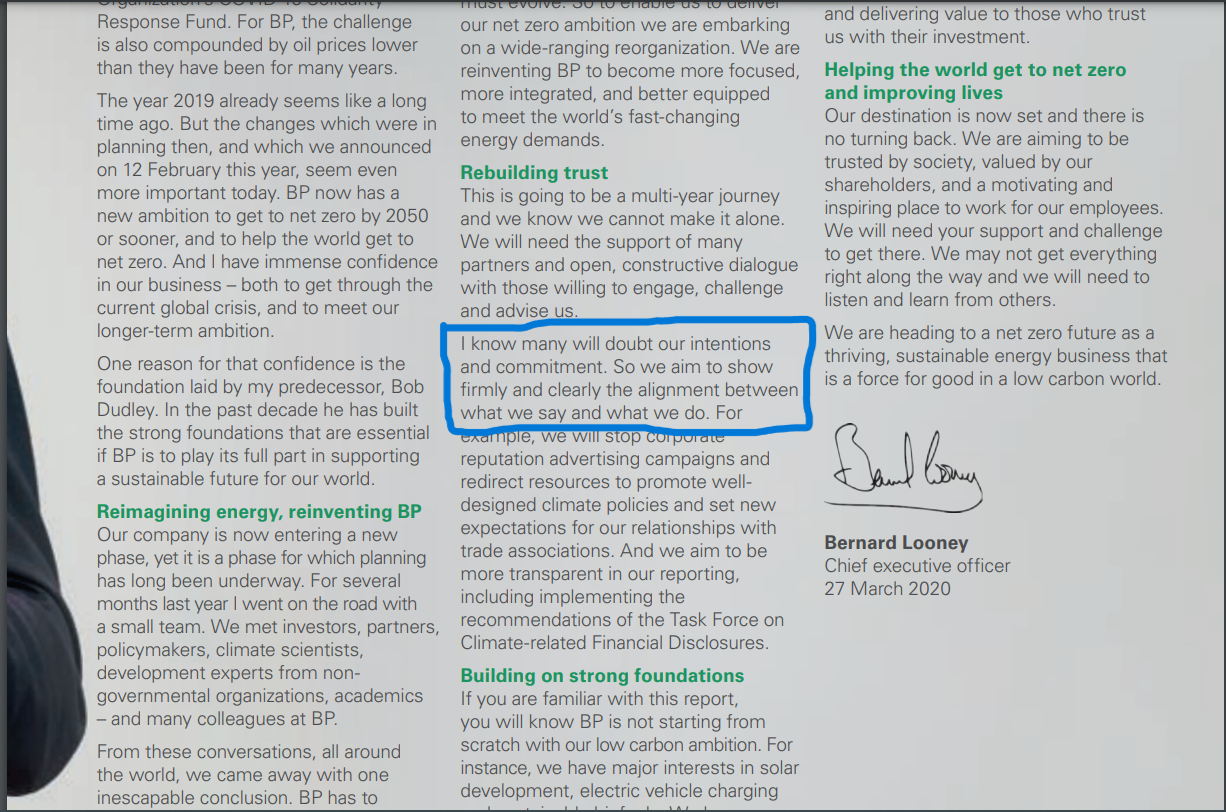

In March 2020, BP released its Sustainability Report 2019. In his first Forward to the Report as CEO, Bernard Looney stated (emphasis added):

BP now has a new ambition to get to net zero by 2050 or sooner, and to help the world get to net zero.

As our purpose and ambition have changed, BP itself must evolve. So, to enable us to deliver our net zero ambition we are embarking on a wide-ranging reorganization.

Looney’s Forward also contained a section titled “Rebuilding Trust”. We highlighted the relevant portion of Looney’s message in the screenshot below:

But by February of this year (less than three years after Looney’s Message), like Blackrock, BP had a significant change of heart about its own intentions. As Bloomberg noted in a February piece (emphasis added):

While the British company said it was doubling down on the transition to cleaner energy with an additional $8 billion of spending to 2030, it will ramp up investments into fossil fuels by the same amount. By the start of the next decade, the company will have higher emissions than previously promised, with oil and gas output down by 25% compared to 2019, compared with its old target for a drop of as much as 40%.

“We’re going to invest more into today’s energy system,” BP Chief Executive Officer Bernard Looney said in an interview on Tuesday. “And that, of course, is a hydrocarbon system.”

As one might imagine, this did not please the world’s environmentalists, regressive “progressive” Charlaticians, and climate activist scientists. You could hardly blame them for pointing out the absurd hypocrisy - except for the fact that their own actions helped cause it.

As it turns out, BP’s about-face on oil and gas production was not unique among London-based global energy companies. In its 2019 Sustainability Report, Shell made similar ambitious climate commitments. Given the events in a Dutch court in 2021, Shell’s newly announced return to capital investment in traditional fossil fuels is even more noteworthy.

In 2019 Milieudefensie, the Dutch wing of the Friends of the Earth, sued Shell to force the company to reduce its CO2 emissions 45% by 2030 (compared to 2010 levels) and to zero by 2050, in line with the Paris Climate Agreement. In May of 2021, a District court at The Hague ruled in favor of the plaintiff who, as you might imagine, was thrilled.

Shell appealed the verdict (the appeal is pending). In the meantime, the same physics and economic reality awakening that seemed to afflict BP spread to Shell.

Four months after BP announced additional fossil fuel investments, Shell did the same despite the pending appeal of The Hague District Court case. Euronews.com summarized the not-so-stunning reversal in a June piece:

Shell is the latest fossil fuel company to scale back on its climate change pledges in order to increase payouts to shareholders. The oil and gas giant announced yesterday that it is dropping plans to cut oil production each year for the rest of the decade.

Shell now says that production will remain stable until 2030, and it will invest $40 billion (€36.7 bn) in oil and gas production between 2023 and 2035. That’s compared to between $10bn (€9bn) and $15bn (€13.7bn) in ‘low-carbon’ products like biofuels, hydrogen and carbon capture and storage.

We doubt the pair pictured above had the same expression on their faces when they heard the news.

The U-turn on ESG is not unique to Wall Street titans and global energy firms trying to play both sides of the fence (and doing so poorly). The global insurance industry has seen its share of backpedaling. In the space of about two years, some of the world’s largest insurers and reinsurers formed an alliance to signal their green virtue (and starve out of favor energy of risk capital), then most fled their own sinking ship like rats at the first storm.

In summer of 2021, the United Nations Environment Programme (UNEP) proudly announced that eight global insurers and reinsurers had united to form the Net-Zero Insurance Alliance (NZIA). In its announcement, UNEP noted that (emphasis added):

“..as founding members, (the firms are) committing to transition their insurance and reinsurance underwriting portfolios to net-zero greenhouse gas (GHG) emissions by 2050.”

At its height, NZIA membership included 30 or more major global insurers and reinsurers. But just like Blackrock, NZIA came under pressure for weaponizing ESG against out of favor industries (read: fossil fuels) and sacrificing pensioner’s funds for political purposes. NZIA’s “alliance” did not hold up well when 23 Attorney Generals from Republican states fought back in May of this year using the threat of state and federal “anti-trust” violations.

The fact that several credible sources suggested anti-trust law could not successfully be used against insurers in such an alliance did not inspire confidence. By June, membership in the NZIA went from a prestigious badge of Green Virtue Honor™ to a Scarlet Letter for many of the members. Reuters recounted the initial wreckage as follows (emphasis added):

A United Nations-convened climate alliance for insurers suffered at least three more departures on Thursday including the group's chair, as insurance companies take fright in the face of opposition from U.S. Republican politicians.

At least seven members of the Net-Zero Insurance Alliance (NZIA), which launched in 2021, have now left including five of the eight founding signatories.

Zurich, Lloyds of London, AXA, Swiss Re, and Hannover Re are among the many well-known global insurers who have left the NZIA. At this writing we are not certain exactly how many members remain. Below is a screen shot of the eleven insurers shown on the NZIA website at the time of publication:

This year, a number of major electric utilities seem to have seen the light. More than a few have begun to strategically shed their taxpayer funded Rube Goldberg “renewable energy” machines, including Duke, AEP and ConEd. Industry experts anticipate even larger portfolios of wind and solar assets to hit the market in the near future.

A July 3rd Wall Street Journal article noted that “Each has said it plans to use the billions of dollars in proceeds to modernize the power lines and other infrastructure that supply electricity for their utility businesses.” Industry publications point to growing investor concern, high interest rates, energy market volatility and other drivers as the cause of the divestitures.

In November 2022, Siemens Gamesa (now part of Siemens Energy) reported a loss of $943 million for its fiscal year ended September 30th due to serious and widespread problems with its wind turbines. By summer 2023, the company was hemorrhaging market capitalization. As a CNBC article from April had noted earlier, Siemens was not alone, as GE, Vestas and other wind energy “leaders” face similar woes.

In addition to empirical reality blowing the shine off the “wind is cheaper” rhetoric, with the exception of Tesla, electric vehicle (EV) makers are not faring much better. A Forbes article this week recounting Ford’s quarterly earnings detailed the red ink (emphasis added):

Ford’s nascent EV division recorded $1.8 billion in sales and a loss of $1.1 billion - year-ago comparisons aren’t available as the operation is still so new.

The loss was expected - it takes a lot of money to get started with the EV transition - but what really got investors’ backs up was that Ford now predicts it will lose $4.5 billion on the Model e division in 2023, which is up a hefty amount from its $3 billion loss guidance.

It is becoming increasingly difficult, if not impossible, to hide the consequences of the West’s energy and environmental policies of the last two decades. Large corporations who have held themselves out to be ESG leaders are having their rhetoric and commitments tested by reality. Instead of reading their lips, watch their actions.

We’re grateful for your “likes”, your “shares” and your subscriptions. They’re helping us grow. And we eagerly look forward to your comments! Special thanks to our Subscribers, almost 1,000 strong and growing!

Great article MENTAL. I always thought the ESG movement was just another wall street scam to syphon money out of the pockets of the retail plebs. Get a teenage girl (Greta) to scream hysterically about her future, the adults in the room nod their heads, the bankers then provide the 'adults' with an avenue to feel better about themselves while allegedly saving the children's futures. Then, a cottage industry of parasitic consultants evolves to help the bankers fleece the public more efficiently before turning their attention to blackmailing major corporations to make generous tithes for their sin of carbon production.

To quote Will Ferrell from Zoolanders, "Does anyone else notice this? I feel like I am on crazy pills."

I'm going to enjoy this for a few minutes. Until they find another way to rip us off, and they certainly will. The nicest part? It makes THEM look bad instead of the rest of civilization! They are a bunch of rich, spoiled, stupid, and immature babies.