Not Laffan Now

One serious attack on a single Middle East LNG export facility and the EU's self-inflicted energy crisis gets even worse.

“It was quite simply a serious strategic mistake to phase out nuclear energy.” – German Chancellor Friedrich Merz

At a breakfast meeting during a NATO Summit in Brussels in July 2018, President Trump expressed his displeasure to America’s European allies the riot act for Europe’s and in particular Germany’s dependence on Russia natural gas. At the time, Russia already supplied over 50% of Germany’s gas demand.

In an address two months later at the United Nations General Assembly in New York, Trump echoed the warning he had delivered in Brussels.

“Germany will become totally dependent on Russian energy if it does not immediately change course.”

The members of the German delegation visibly laughed and smirked. Forty months later when Russia invaded Ukraine, Germany and Europe came begging to Trump’s successor, Joe Biden (and Canadian Prime Minister Justin Trudeau), for liquified natural gas (LNG).

At the time, Germany consumed fifteen times more natural gas than it produced domestically, nearly double from 2010 around the time its Energiewende began to take its present, destructive form. Today, Germany consumes 22 times more natural gas than it produces.

While Germans were laughing at Trump in 2018, the EU 27 bloc as a whole was consuming more than six times the amount of natural gas it was producing. (By the end of 2024, that multiple had increased to over 11!)

When Russia invaded Ukraine in February 2022, global oil and natural gas prices spiked. That summer Europe scrambled to secure LNG imports from wherever it could to make up for lost Russian supply even before western interests destroyed the Nordstream 2 pipeline that September. The premium paid by the EU to secure whatever natural gas it could obtain priced out developing countries like Pakistan and Bangladesh, leading to electricity blackouts for millions in those two countries.

When natural gas prices at the benchmark Dutch TTF trading hub hit €340/megawatt hour that August, the Germans and Europeans were not laughing any more. Converted to U.S. dollars per million BTUs (mmBTU), the figure was about 10 times higher than the price of natural gas at the U.S. Henry Hub benchmark.

The damage from higher energy prices to Germany, Europe’s largest economy, has been substantial. The German economy contracted in six of eight quarters between Q4 2022 and Q4 2024 with the other two quarters registering 0% growth. Deindustrialization across the chemical, fertilizer, automotive and other industrial sectors has cost hundreds of thousands of jobs and large numbers of plant closures.

The war in Iran commenced by Israel and the U.S. in the early hours of March 1 created a similar set-up to summer 2022 for oil and natural gas price spikes, when global supply was constrained by war and Russian sanctions. Only this time, the situation is even more dangerous for energy markets and Europe in particular. Iran’s counterattacks almost immediately in response targeted not only Israel and American military targets, but also its Gulf neighbor’s interests, including energy infrastructure.

When markets opened this Monday, month forward natural gas prices at the TTF briefly traded for nearly double the €32/megawatt hour (€/Mwh) February 27 market closing price, and front month Brent Crude traded briefly at nearly $120/barrel, a spike of over 60% from its pre-war market price. Finance officials from G7 nations calmed markets by expressing willingness to dig into the strategic reserves (equal to ~90 days of net imports) held by the International Energy Agency’s (IEA) 32 member nations. The U.S. appeared to enthusiastically support the idea, recommending a release of 300 – 400 million barrels or about a third of the roughly 1.2 billion barrels held by IEA member nations.

Oil is a fungible global commodity that can be loaded right onto tankers in the form from which it is pumped out of the ground. As such, U.S. benchmark West Texas Intermediate (WTI) crude caught the Brent crude bid and spiked to near $120/bbl before the G7 and IEA’s signals calmed international oil markets. But unlike European markets, the spike in the U.S. Henry Hub benchmark natural gas price from the start of the Iran war to when U.S. markets closed this Monday afternoon was limited to ~22%.

Unlike oil, natural gas cannot be pumped out of the ground and put on cargo ships. It must be liquefied first. As such, no “strategic natural gas” reserve exists anywhere in the world.

Iran is shooting missiles at its Arab neighbors and attacking them with drones, hitting the world’s largest LNG liquefaction facility in Qatar and source of ~15% of Europe’s imported natural gas with a drone only two days into the war. Having learned nothing from its last self-inflicted energy crisis in 2022, the European Union (EU) now finds itself on the brink of another, possibly worse, situation four years later.

Why is the U.S. in a better structural position to weather the storm it created in energy markets when it joined Israel and attacked Iran? How might the combination of EU’s domestic paucity of hydrocarbon energy production relative to its consumption and current global LNG supply make this situation different than 2022? And which single LNG liquefaction and export facility on the shores of the Persian Gulf is one missile or drone attack away from sending European natural gas levels back into the hundreds of Euros per megawatt hour range just like August of 2022? Let’s do some situational recon from a safe distance as the projectiles continue to fill the skies and drones swarm over the Middle East.

We begin with a reminder just how dependent the EU has chosen to become on foreign energy imports by virtue of its integrated environmental, energy and economic policies. As we noted in Help Me Help You back in November and the Doomberg team well before us, the EU consumed almost 39 exajoules of hydrocarbon energy in 2024 but produced less than 5 exajoules from within its own borders. (For reference, an exajoule contains the energy equivalent of about 160 million barrels of oil.)

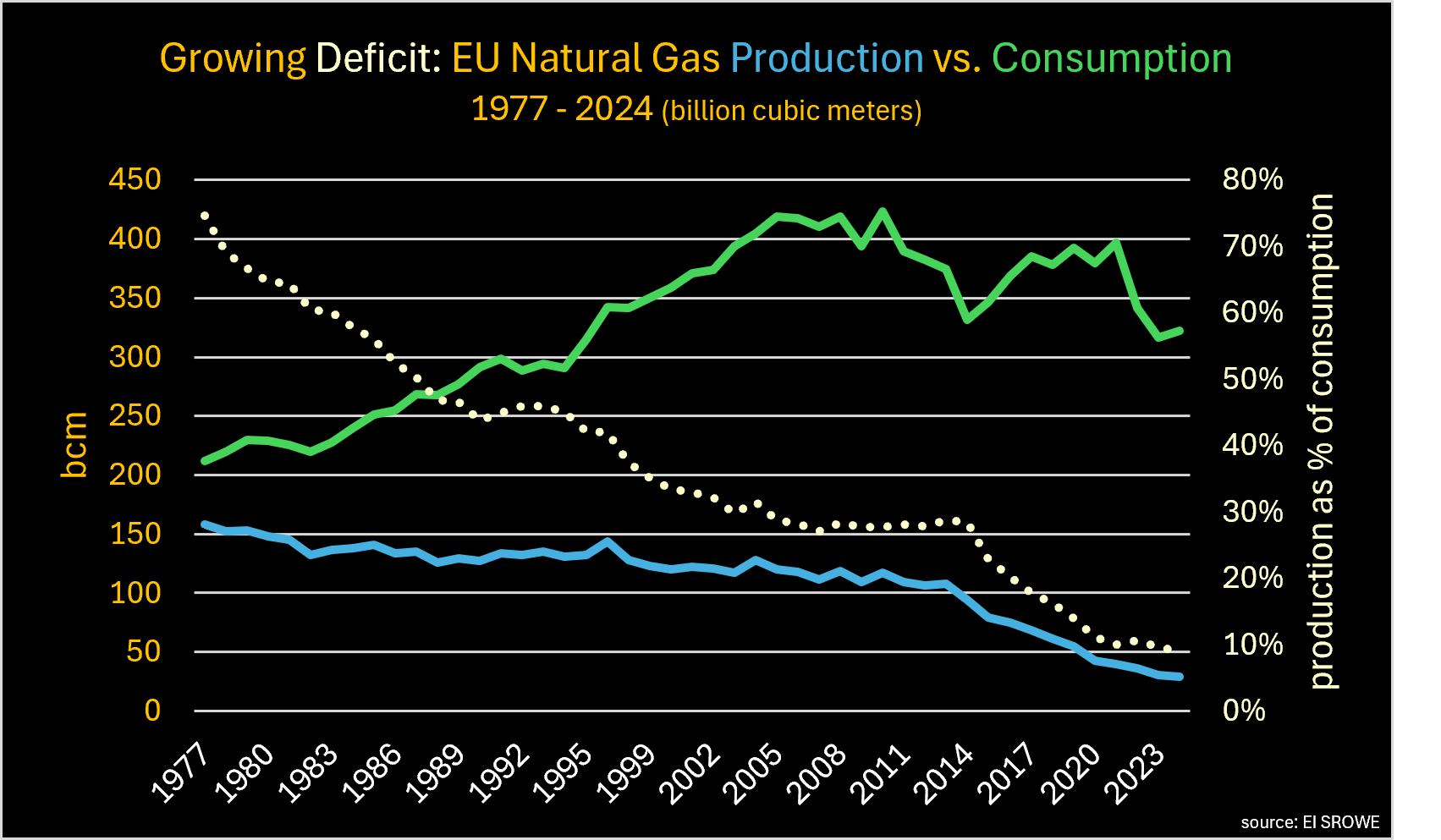

In 1977, the 27 members of the current European Union produced about 75% of the natural gas their economies consumed. But ever since that era – long before “climate change” drove western energy policy – their production began to wane. The gap between domestic natural gas production and consumption shown in the graph below has been growing steadily ever since.

When the EU took a victory lap for the Paris Agreement on “climate change” in 2015, the bloc was still producing almost 25% of the natural gas it consumed. By the end of 2024, the figure had dropped to less than 10%.

The EU chose to become increasingly dependent on foreign hydrocarbon energy imports. The Paris Agreement, Germany’s Energiewende and similar policies other western European countries held out as virtuous and “leading the world on climate change” were deliberate, and their leaders and citizens quite proud to enact them.

While Europe might not be blessed with America’s geologic inheritance, it does not lack for natural gas fields. As German Substack writer Brawl Street Journal commented in a March 3rd Note (emphasis ours):

“The potential for European gas production looks enormous on paper. According to a 2013 energy study by Germany’s Federal Institute for Geosciences and Natural Resources (BGR), Europe’s technically recoverable gas resources amount to 21 trillion cubic meters (tcm). This volume would cover the EU’s entire gas demand for 65 years.”

According to Brawlster’s analysis, the roughly €100 billion spent by the EU each year between 2021 and 2023 on “renewable energy” subsidies could have underwritten 270 billion cubic meters (bcm) of domestic natural gas production – about 85% of EU’s current gas consumption levels - annually.

Instead, while engineering a hydrocarbon energy deficit that (unsurprisingly) undermined their economies, political stability, and their citizen’s living standards, EU political “leaders” harangued U.S. politicians and Presidents for their lack of similar “leadership.”

The U.S. is blessed with more advantageous geology, and the U.S. chose a different policy path. The technological innovation its entrepreneurs (like U.S. Energy Secretary Chris Wright) developed that unlocked vast stores of oil and natural gas was not subsequently prohibited by law, as it was in most of Europe.

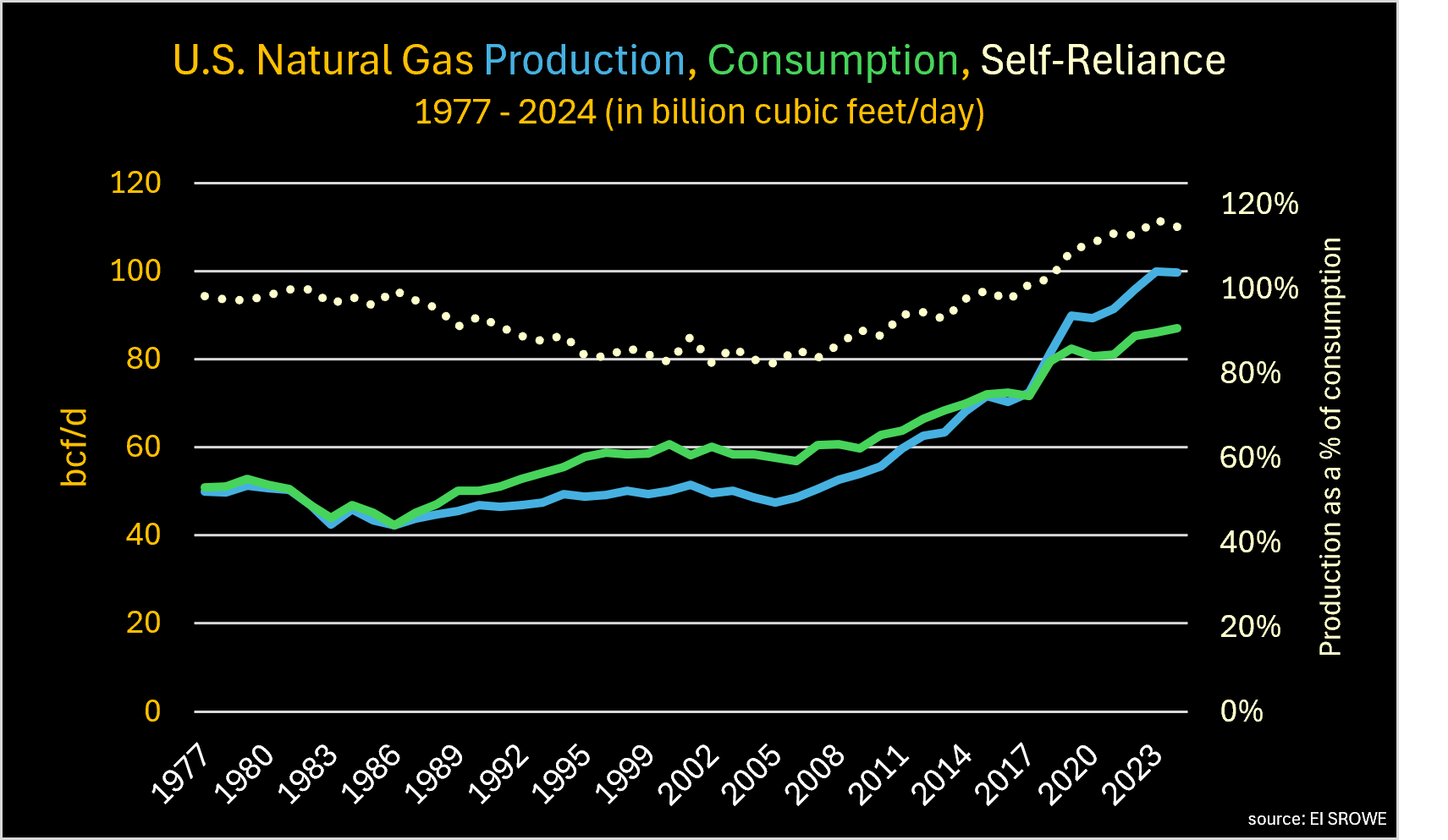

Thanks to that geology and the relentless incremental improvements in fracking technology, the U.S. is the world’s largest producer of liquid petroleum products and natural gas. Today, America produces over 20% of global petroleum liquids and ~25% of global natural gas.

After bottoming out in 2005 at 82% of domestic consumption, in 2017 American natural gas production equaled domestic consumption for the first time since 1986 thanks to the U.S. fracking boom. Despite domestic consumption growing by nearly 75% since 1977, today U.S. natural gas production equals ~115% of consumption. If the German clowns laughing at Trump’s UN speech in 2018 had any self-awareness they would, in retrospect, acknowledge that without that growing surplus since 2017, the self-inflicted mess in which Europe has found itself since 2022 would be much worse today.

Compare American domestic production, consumption, and self-reliance in the graph below to that above for Europe.

The result? Europe is, as Doomberg is fond is stating, an “energy vassal.” The U.S. is an energy superpower and, unlike Europe (or the UK), its energy security is not in question.

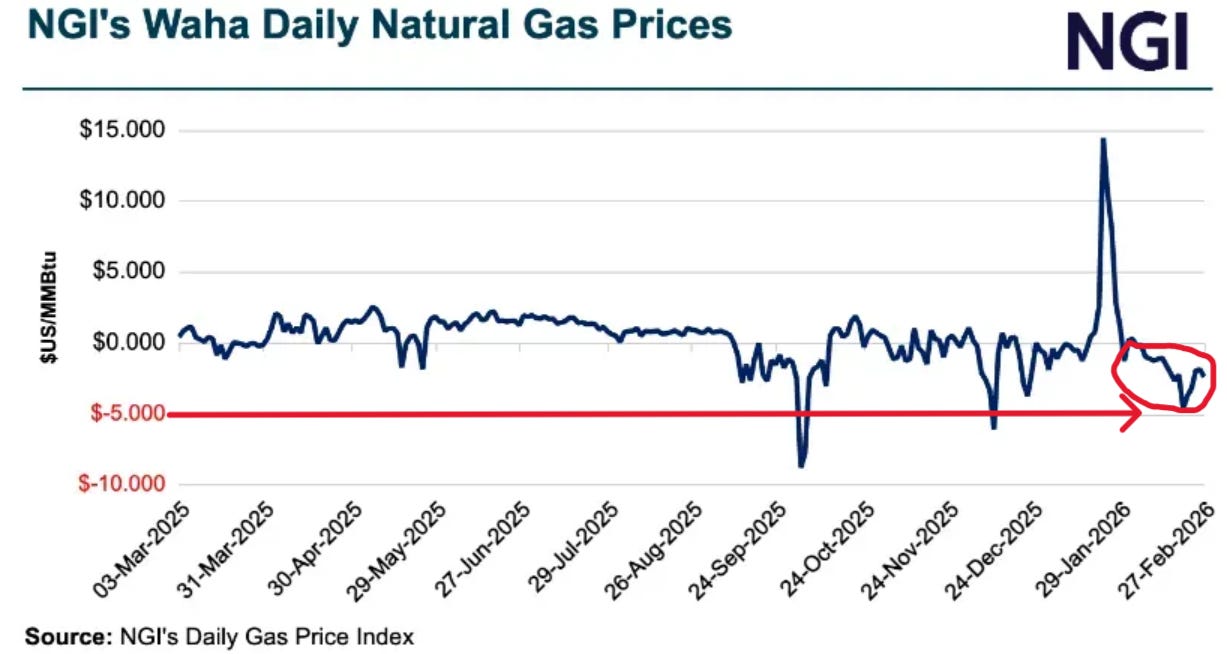

For perspective, consider that the day before Israel and the U.S. began bombing Iran, natural gas at the U.S. Henry Hub closed at $2.86/mmBTU. Converted from €/Mwh to $/mmBTU, the closing price that day at the Dutch TTF hub was nearly four times U.S. prices at just under $11/mmBTU. But only four days before the war began, natural gas prices at the Waha trading hub in the U.S. Permian basin set a new record (emphasis added):

“In the cash market, average prices at the Waha Hub fell to minus $4.56 per million British thermal units (mmBtu) for Monday, down from a negative $2.16 for Friday.

That was a record 12th day in a row that Waha prices closed below zero. The prior record was 10 days in June 2025.”

While the EU allowed a steadily growing, five-decade deficit to occur between domestic natural gas production and consumption, America steadily closed its small deficit and turned it into a surplus. This reality puts both in vastly different circumstances given the developing crisis in the Middle East.

Several other important differences versus the 2022 global energy crisis make the war in Iran more challenging for an already struggling Europe. While significant new LNG export capacity is coming online this year and next throughout the world, most of the 2026 completions will not occur fast enough to alleviate shortfalls sure to develop over the next few weeks unless the war ends quickly. The U.S. exports the most LNG globally but most of its capacity is committed under long-term contracts.

Russia, which has been providing increasing LNG cargoes to the EU even as the bloc has reduced imports of Russian pipeline gas, has the capacity to provide some relief. But instead, President Putin is giving the EU an ominous signal.

As Doomberg noted in No Laffan Matter, last week:

“In comments made on Wednesday, the Russian president hinted that instead of helping his adversaries, he might take the opportunity to put the screws to them.” (emphasis added):

“Russian President Vladimir Putin said his country will consider ending most sales of natural gas to Europe in favor of more promising alternative markets.

The European Union plans a gradual ban on imports of both Russian pipeline gas and liquefied natural gas by late 2027. In this light, the Russian leader said he would instruct his government to assess redirecting supplies away from the bloc so that officials could work on the issue with companies.

Other markets are opening now,’ Putin said on state television on Wednesday. ‘Maybe it’s better for us to end supplies to the European market right now? To go to those markets that are opening now and get a foothold there.”

As if these risks and complications were not enough, consider that the theater for the Russia – Ukraine war did not constrain the flow of crude oil or natural gas through natural chokepoints in dangerous neighborhoods. In fact, sanctioned Russian oil has made its way via a fleet of shadow tankers to refineries in India and China, (at a discount) - without risk of attack in a narrow straight in the middle of the conflict - since it invaded Ukraine and continues to do so.

But about 20% of global oil consumption and a quarter of seaborne crude trade flows through the Strait of Hormuz, which is effectively shut down and now sits squarely in the middle of a war zone. About $50 billion of hydrocarbon energy products flow through the Strait each month, with Iran’s share accounting for around 10%.. The EU must hope that somehow the Strait of Hormuz opens quickly.

But perhaps the biggest risk of a serious energy problem for Europe relates to the bloc’s natural gas supplies, where storage is already dangerously low at or below 30% of capacity (about a third below normal) coming out of winter. The world’s single largest LNG liquefaction and export facility sits a chip shot away from Iranian missile and drone launching sites across the Persian Gulf. That reality creates a concentration of natural gas supply risk for Europe, and the facility has already been targeted in this conflict.

Within forty-eight hours of the start of the war, Iranian drones struck QatarEnergy’s Ras Laffan facility. Operating 14 LNG liquefaction trains with a combined nameplate capacity of nearly 110 bcm/year, Ras Laffan is responsible for 20% of global LNG production, and 100% of it has to pass through the Strait of Hormuz.

Ras Laffan sits on the northeast coast of Qatar, a ~100-mile-long peninsula sticking out from the southwest Persian Gulf coast. It sits precariously close to the Strait (~300 miles west) and sits within 120 miles of Iran’s border.

After the attack, Saad al-Kaabi, Qatar’s energy minister and CEO of state-owned QatarEnergy shut down the facility and said, “We don’t yet know the extent of the damage, as it is currently still being assessed. It is not clear yet how long it will take to repair.” Two days after the attack, the company declared force majeure on its LNG contracts, a legal maneuver to head off contract default claims. The same day, Reuters cited “sources saying it may take at least a month to return to normal production volumes.”

LNG liquefaction trains are complex systems, not the type of thing for which one flips the switch and starts producing the supercooled gas and loading it on cargoes ships that afternoon. The process is complicated and 30-50 days for a full assessment, inspection, and pressure vessel testing and cycling would not be unusual.

Within five days of Reuters report, QatarEnergy began offering eleven LNG cargo tankers located outside the Strait of Hormuz for lease. Whether that was a signal about the damage and expected duration of the closure at Ras Laffan or worry about trying to transit their cargo tankers through the Strait is unclear.

The current spot market for global LNG is likely tighter than in the summer of 2022, when Europe scrambled around the world paying exorbitant prices to get it. There may be no more than 2-3 bcf/d of spot market capacity (most of it from the U.S.) to make up for the current loss of Ras Laffan’s 10 bcf/d production.

We close by wondering how much longer the EU can sacrifice the bloc’s energy security, economic competitiveness, and its citizen’s standards of living on the altar of its centrally planned “energy transition” and “net zero” policies and aspirations. Four months ago the U.S. and Qatar sent the EU a clear signal: failure to eliminate penalties of “not less than 5% of global net revenue” and the prospect of civil liability for failing to comply with its Corporate Sustainability Due Diligence Directive (CSDDD) would seriously threaten energy imports from producers with alternative markets. Yet so far, nothing but crickets from the EU about the CSDDD.

At a Nuclear Energy Summit in Paris yesterday, European Commission President Ursula von der Leyen not only (belatedly) acknowledged the self-induced problem but did an about face on nuclear energy (emphasis added):

“Industrial competitiveness is increasingly determined by who can best produce, transport, store and use abundant and affordable electricity.

Now, Europe is neither an oil nor a gas producer. For fossil fuels we are completely dependent on expensive and volatile imports. They are putting us at a structural disadvantage to other regions, and the current Middle East crisis gives us a stark reminder of the vulnerability it creates.

But we have homegrown energy sources. Nuclear and renewables. And together they can become the joint guarantors of independence, security of supply, and competitiveness if we get it right now…

…While in 1990 one-third of Europe’s electricity came from nuclear, today it’s only close to 15%. This reduction in the share of nuclear was a choice, and in hindsight it was a strategic mistake for Europe to turn its back on a reliable, affordable source of low-emissions power. This should change.

Europe chose the structural disadvantages Von der Leyen acknowledged. Her comments - less than three years after Germany shut down the last of its nuclear power plants in the midst of the last energy crisis – might suggest Europe’s Charlaticians™ are finally beginning to see the error of their ways. But those comments alone will not change the political calculus in the EU any time soon, and any European nuclear renaissance won’t come soon enough to fix the mess they have created.

Will EU “leaders” go through with the CSDDD as planned after being admonished by the U.S. and Qatar - suppliers of 45% of global natural gas - in October and in the wake of what they have now learned twice in four years? Or could this be a convenient and timely opportunity for the EU to begin to climb down from the altar of “renewable energy,” “net zero,” and “climate change?”

Only time will tell. Meanwhile, with Ras Laffan one bad drone or missile attack away from a lengthy closure, European “leaders” may have been laughing at Trump about natural gas security in 2018, but they probably aren’t laffan now.

“Like” this post (whether you actually like it or not) to congratulate us for our 100th post on Substack!

Leave us a comment. We read and reply to all. Refuels the tank here.

Subscriptions to environMENTAL are free, but please consider a paid subscription.

Share this post. Helps us grow. We’re grateful for the assist!

And then there's this (highly predictable) article headline in my morning scan of the WSJ:

"Europe’s New Energy Crisis Will Mean a Bull Market in Renewables"

It never stops. High fossil fuel prices only seem to embolden the faithful, rather than considering their views may be counterproductive.

Countries led by politicians making decisions, based on their own egos, to wave the self righteous climate change victory flag. When all they've really done is outsourced the problem to countries that don't give a s about "saving the planet". I find it disgusting really. No different than US cities/states out sourcing their garbage to poor countries or moving their manufacturing over to China all the while claiming how important the climate is. Yeah, right