Big Evoil Punches Back

"The height of strategy is to attack your opponent's strategy" -Sun Tzu

In December 2020, a newly formed activist investment fund called Engine No. 1 purchased $40 million worth of Exxon Mobil stock. Shortly after taking the position, its Founder Christopher James penned an open letter to the Exxon Board of Directors criticizing Exxon’s Return on Capital Employed (ROCE).

Exxon was about to close the books on a disastrous 2020. Covid-19(84) had decimated global economies and with it the earnings of major oil companies. For a few days in March of that year, West Texas Intermediate oil actually traded at a negative cost per barrel. In early 2021, Exxon reported a loss of over $20 billion for 2020.

As the world’s largest non-state energy company, by the time Exxon’s board received James’s letter in late 2020, the company had already become the big prize for environmentally focused activist investors. And the world’s leading climate villain.

James’ letter to Exxon’s board proposed widespread reforms and proposed a slate of four independent directors with experience in the energy industry. In the fifteen years prior to Engine No. 1’s effort, American and European publicly traded oil and gas companies had received a barrage of activist investor proposals, most of which were focused on CO2 emissions reduction and failed to gain enough shareholder votes to move the needle.

Christopher James and Engine No. 1 chose a different tact than their predecessors. They successfully convinced some of Exxon’s largest shareholders, including (ESG Maven and) Blackrock CEO Larry Fink, Vanguard, and State Street, to vote for their proposal.

When the smoke cleared after Exxon’s shareholder meeting in May of 2021, despite holding a mere 0.02% of Exxon shares, Engine No. 1 candidates had won three seats on Exxon’s Board of Directors. The usual legacy media Climate Corps hailed the win as a transformational, “David beats Goliath” victory.

Engine No. 1’s win naturally inspired other climate activist investors, including several who had tried unsuccessfully for years to impose their proposals on Exxon under the pretense of the interest of shareholders. Two of those firms, Arjuna Capital and Follow This, have submitted fourteen shareholder proposals to Exxon dealing with “climate change” in some form just in the last eleven years.

Arjuna Capital is a U.S. registered investment advisor (RIA) based in Durham, North Carolina with offices in Massachusetts. On its website, Arjuna touts “enlightened investing” and displays its model as “Divest” (from fossil fuels), “Invest” (“sustainable” solutions) and “Engage in Corporate Change” (ESG shareholder activism).

Follow This is an Amsterdam-based non-profit association which claims to have over 10,000 members. The “About” page on its website describes its strategy:

“Follow This changes the system by entering it. We empower shareholders to vote for change at Big Oil shareholders’ meetings (AGM). We do so by filing AGM resolutions that put climate action on the ballot.”

The two activists engage in different tactics. As an environmental activist RIA, Arjuna represents clients whose holdings in target energy companies reach the necessary Securities and Exchange Commission (SEC) threshold to enable the firm to bring shareholder proposals on their behalf.

Follow This solicits donations through its website from interested parties which the organization uses to purchase enough shares in target energy companies to meet those same SEC thresholds. It purports to assign each share to the individuals making the contributions. The contributors give the mandate and Power of Attorney to Follow This to vote the shares, effectively transferring rights to bring shareholder proposals to the organization.

To date, all of the shareholder proposals submitted to Exxon by Arjuna and Follow This which were not withdrawn or excluded on technical grounds were rejected. Most were defeated by large margins.

The rejections have not discouraged Arjuna Capital and Follow This who, on the surface, seem to have altruistic motives. But if there is a form of shareholder activism more hellbent on destroying capital, value, and more important products and/or services demanded by global society than their form of environmentally driven shareholder activism, we have yet to find it.

On December 14, 2023, Arjuna Capital submitted its latest shareholder proposal to Exxon for consideration at its May 2024 annual shareholder meeting. The following day, Follow This joined Arjuna’s proposal as a co-filer. (The year prior, Follow This submitted a nearly identical proposal and Arjuna joined it as a co-filer.)

Exxon’s patience with more than a decade of onslaughts from climate change-focused activist investors using SEC’s loose “shareholder proposal” rules and guidance as a weapon to destroy the company finally wore thin. On January 21, 2024, it sued Arjuna Capital LLC and Follow This in the North Texas Federal District Court, seeking a declaratory judgment that the company may legally exclude their proposals from its upcoming 2024 shareholder meeting.

If Exxon succeeds, it could set legal precedents that would send shockwaves through environmental shareholder activist circles. What are the legal bases for Exxon’s claims? How did Arjuna and Follow This respond to the lawsuit? And where does the matter stand?

We begin with Exxon’s initial response to the Arjuna/Follow This proposal and a brief overview of the issues at hand. Eight days after receiving the proposal, Exxon notified both proponents of procedural and eligibility deficiencies. It then notified the SEC that it intended to omit the proposal from the proxy statement it plans to issue for its May 2024 annual shareholder meeting. (SEC rules require corporations to notify proponents of deficiencies when they intend to omit the proposal from their proxy statements prior to notifying the SEC.)

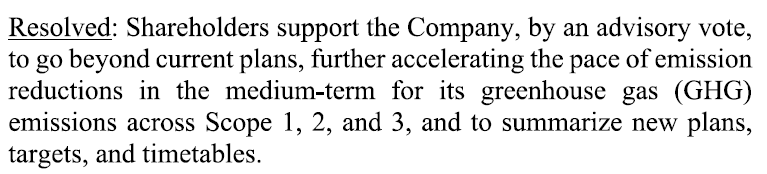

The 2024 Arjuna/Follow This shareholder proposal targets the U.S. oil and gas industry’s biggest prize, using what it perceives to be among its biggest vulnerabilities: It requests that Exxon Mobil accelerate the pace of greenhouse gas emissions reductions in the medium-term, across not only Scope 1 and Scope 2, but Scope 3.

For readers unfamiliar with the different emissions “Scopes”, each relates to a different source associated with a company’s business. Scope 1 emissions relate to sources a company owns, operates, or controls. Scope 2 relates to indirect emissions from services like utilities or other sources such as the electricity, steam, heating, or cooling purchased by the company. Scope 3 includes indirect emissions that may result from activities up and down the value chain but not owned or controlled by the company.

Because Scope 3 emissions for major energy companies include those resulting from consumers’ legal use of the company’s products, they include the burning of gasoline and diesel by motorists, commercial trucking, cargo ships, aviation, power generation, process heat, and essentially all other end-use combustion of the products they sell. Environmental activist investors understand the implications of this all too well and have seized upon it as a key lever to force the five largest U.S. and European publicly traded oil and gas firms to turn their business models upside down. Exxon Mobil is the only one of the five major Western oil companies (along with Shell, BP, Chevron, and France’s TotalEnergies) without Scope 3 emissions targets.

Forcing major oil and gas concerns to reduce their “Scope 3” emissions is functionally equivalent to forcing farmers to account for and reduce methane emissions from the humans who consume their food. Just as farmers can do virtually nothing to change the degradation properties of meats, grains, fruits and vegetables in your gut, there is nothing oil and gas companies can do to change the carbon-hydrogen molecular structures of hydrocarbons on planet earth. When used as intended, they combust, and the combustion process releases CO2.

To simplify their arguments, Arjuna Capital and Follow This want shareholders to believe that Exxon can continue to sustainably (actual definition intended) grow revenue and earnings by shifting their entire business to “alternative” energy sources. This would require Exxon (and the other major oils) to replace petroleum hydrocarbons (principally oil and natural gas) with some combination of biofuels derived from crops, algae, synthetic fuels, and hydrogen at a scale that is presently unrealistic, unachievable, and not even necessarily desirable.

Even if doing so were possible on time scales that would not wreck the world economy and living standards (it is not), the world would still produce crude oil for a dizzying array of products critical to society. The services provided to humanity by the crude oil and natural gas produced every day by the five major oil companies targeted by Arjuna and Follow This cannot be replaced in the short-to-medium term by any combination of wind, solar, biofuels, and hydrogen alternatives. We believe that Arjuna Capital and Follow This are smart enough to understand these realities.

The Introduction in Exxon’s complaint begins:

“Most shareholders invest in companies to help the companies grow and see a return on their investment. But Arjuna and Follow This are not like most shareholders.”

Follow This proudly articulates its “Goldilocks Trojan Horse” strategy for changing the business model of energy companies on its website. See if you can find the “good faith intent” to help Exxon grow and for shareholders to achieve a return on their investment by what we have highlighted below:

It is just as difficult to find alignment with the interests of retail and institutional shareholders in Arjuna’s articulated strategy:

For glaring examples of the divergence between the interests of Arjuna/Follow This and those of Exxon’s shareholders, look no further than Engine No. 1’s recent votes on such matters. In 2022, Engine No. 1 voted against Follow This’ shareholder proposal calling for Exxon to reduce its Scope 3 emissions. In October 2023, all three of Engine No. 1’s successful 2021 Board picks voted in favor of Exxon’s $60 billion acquisition of Permian basin oil and gas giant Pioneer Natural Resources.

SEC rules provide thirteen bases for corporations to legally omit shareholder proposals from their proxy statements for a vote at their annual shareholder meeting. Exxon’s notice to the SEC, as well as its lawsuit, focuses on two of these, the “ordinary business rule” and the “resubmissions” rule (for interested readers, these are found at 14a-8, subsection (i), items (7) and (12) ). The former restricts proposals attempting to micromanage a company’s ordinary day-to-day business. The latter restricts submission of proposals substantially the same as prior years.

Regarding the “ordinary business operations” exception, Exxon argues that, by demanding that the company go beyond current plans and set more aggressive medium-term targets for Scope 1, 2, and 3 emissions:

The “resubmissions” rule allows corporations to omit the proposal if two conditions are met. First, the proposal must address substantially the same subject matter as a proposal included in proxy materials within the previous five years and voted on in the prior three years. The second relates to the share of votes the proposal received. In this case, if the proposal was voted on twice within the last three years and received less than 15% of votes in the most recent proxy, it may be omitted.

Compare the Arjuna/Follow This 2023 shareholder proposal…

To their new 2024 proposal…

Are they substantially the same? In the most recent vote (2023) the Arjuna/Follow This proposal was defeated by a vote of 89.5% to 10.5%. A similarly worded proposal advanced by Follow This in 2022 was defeated by a vote of 72.9% to 27.1%.

Exxon argues that the 2022 and 2023 proposals address “substantially the same subject matter” and, because the 2023 proposal only garnered 10.5% of the votes, they are entitled to omit the 2024 proposal.

Exxon’s lawsuit asks the North Texas District Court to rule that it may legally omit the Arjuna and Follow This shareholder proposals under these two specific SEC rules. Why would Exxon seek legal relief from a Federal Court to impose SEC’s rules? Because the company believes that, with respect to environmental activist shareholder proposals, the SEC has been applying Rule 14a-8 in a conveniently arbitrary, selective, and destructive manner. In its filing, Exxon states:

How did Arjuna Capital and Follow This react to being sued by the biggest U.S. target of their opposition and opprobrium? Whether it was the expense of fighting a Fortune 100 corporation or the desire to avoid having a federal court set a precent deadly to its objectives, eight days after Exxon sued Arjuna and Follow This, both parties withdrew their proposal, promised not to refile it, and retreated to the safety of their rhetoric.

But Exxon was not done with the matter. Rather than withdrawing their complaint in the North Texas District Court, they simply withdrew their motion for an expedited hearing. Last Friday, the company stated, "We believe there are still important issues for the court to resolve. There is no change to our plans, the suit is continuing.”

Exxon’s refusal to drop the lawsuit likely constitutes a financial “oh sh#t” moment for Arjuna and Follow This. But you wouldn’t know it from Arjuna Managing Partner and Chief Investment Officer Natasha Lamb, who failed to see the irony in her statement complaining about Exxon’s tactics when she commented (emphasis added):

"There is no basis for Exxon to continue this attack once the proposal was pulled back. This amounts to tactics of intimidation and bullying to silence investors.”

We suspect we’re not the only ones who find irony in environmental shareholder activists complaining about “intimidation and bullying”.

Follow This Founder Mark van Baal offered similar sentiments:

"Given Exxon's preference to fight a battle in court rather than allow shareholders the freedom of a vote at its annual meeting, we decided to withdraw the climate proposal. Now that we have withdrawn and promised not to refile the proposal with Exxon, the company has no reason to continue the lawsuit.”

Given that Arjuna and Follow This withdrew their shareholder proposal, but Exxon did not drop the lawsuit, last Friday Judge Pittman ordered Exxon to file an update detailing its outstanding claims and issues before the court by Monday. The update Exxon filed Monday evening begins:

ExxonMobil filed this case because year after year Defendants submit shareholder proposals under the federal securities laws to advance their personal agenda at the expense of ExxonMobil’s shareholders. And there is no good reason to believe they will stop.

Exxon’s Court update references Follow This’ Goldilocks Strategy and the fourteen similar proposals the two defendants have offered over the last eleven years. It notes that the SEC “permits this type of conduct under its current application of the rules”. Exxon alleges that SEC staff interpret securities regulations in a manner that is inconsistent and encourages these types of proposals “designed to disrupt the ordinary business operations of public companies and harm their shareholders.”

Exxon effectively claims the SEC is hiding behind rule interpretations, informal guidance documents, the fact that guidance has no legal force, and that it cannot decide the merits of a company’s position related to shareholder proposals. Since the SEC refuses to apply its own rules equitably, Exxon is asking the court to do it for them, citing the specific rules at issue in this case.

While a ruling adverse to Arjuna/Follow This would only have legal force in the North Texas District (where Exxon is not the only publicly traded oil and gas company), the Court’s ruling would set important precedents and likely be tested in other federal District Courts. As such, the implications of an adverse ruling in this case are potentially severe for environmental shareholder activists.

We close with something we believe few have considered, in particular the environmental shareholder “activists” who now find themselves facing the prospect of a horribly inconvenient, if not devastating, legal precedent.

It is not obvious to us that the perpetrators of such activism have considered the consequences of the pandora’s box they opened, including the possibility that their tactics might be used similarly against “alternative” energy companies they support. Given that the SEC has tolerated all manner of environmental shareholder activism, some of it rather dubious under SEC’s own rules, we will not be surprised if or when a counter activist group turns the tables against some of the world’s largest publicly traded “renewable energy” firms.

For example, Arjuna Capital, Follow This and other activist investors pushing oil and gas firms toward “alternative” energy commonly portray “stranded assets” as a future threat to shareholder interests. Danish Oil and Natural Gas reinvented itself as wind darling Orsted, has recently seen its share price crater, and paid tens of millions to cancel U.S. offshore wind contracts before they could even build the assets to strand them. In one form or another, similar situations apply to Equinor (formerly StatOil), Siemens Energy (who recently received a German government loan guarantee bailout), BP and several other U.S. and European publicly traded companies.

Imagine this scenario: An activist investor group puts forth a shareholder proposal questioning the financial viability of overinvesting in “alternative” energy and dependence on government subsidies. They nominate directors who would reverse the company’s strategies. If the SEC and its foreign equivalents were to apply the same standards to such a proposal received by an Orsted, Equinor, BP, or Siemens Energy as has been applied to oil and gas companies like Exxon, what would happen?

We can only wonder. We don’t suppose environmental shareholder activists have even considered the proposition. But thanks to the Pandora’s box they have opened, we would not be surprised if they found out.

“Like” this post or we’ll make the next one even longer.

Leave us a comment. We’re grateful for your feedback and enjoy the engagement!

Share our work. It helps us contribute to sorely necessary public discourse.

Great article, and an example of what happens when the petulant and the clueless, like Natasha Lamb get ahold of daddy's money: they can be really annoying!

The problem for them is that Exxon is chock full highly educated scientists and engineers and attorneys who have a good grip on the basic Law's of Physics and The Law......and deep pockets.

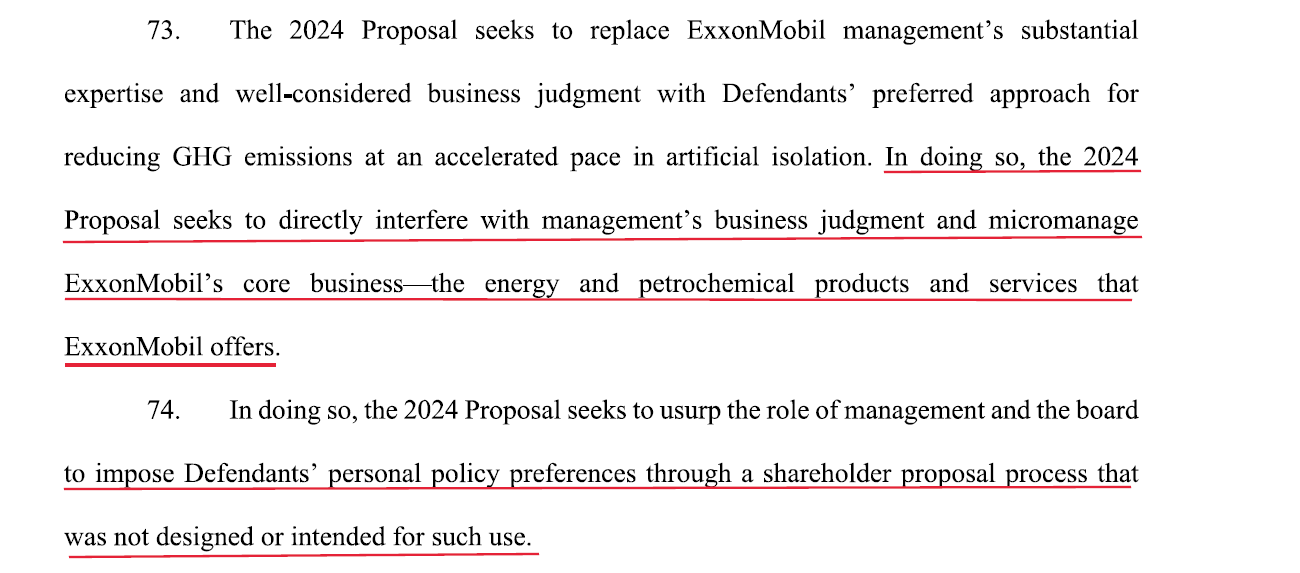

Excellent article. Thanks. I see some unraveling of the environmental activist actions if not agenda and find it heartwarming.